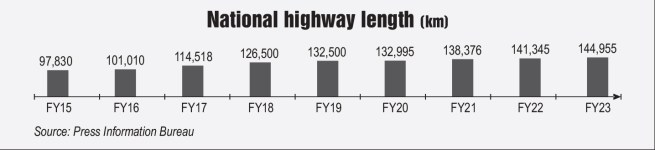

India has a relatively large and diverse transportation infrastructure asset base, a significant part of which is the road network. Over the past three decades, the central and state ministries have played a significant role in the development of roads and highways. This is driven by strategic leaps (Golden Quadrilateral, Bharatmala, etc.) as well as financial innovations such as take-out financing, the 5/25 rule, public-private partnerships (PPPs), and tax holidays. India’s road network is currently the second largest in the world in terms of size.

The Infraverse

What is even more fascinating is the journey towards achieving such scale in the roads and highways space. There have been multiple layers of transformation in this space – be it contractual models, financial instruments, the supply-side landscape or digital initiatives.

It all started by enabling private investment and efficiency through PPPs in the mid-2000s. Within a few years, the secondary market (investment market in the post-construction phase) also started to emerge. Soon after, between 2009 and 2012, PPPs in the sector began to show signs of stress. The build-operate-transfer (toll) model had somewhat encouraged bidding based on speculative parameters such as traffic, rather than efficiency. By 2013, symptoms of a systemic slowdown in highways’ PPP off-take emerged due to multiple factors, including the emergence of non-performing assets, liquidity crises, as well as a significant drop in the project financing appetite and PPPs.

The government quickly realised the issue and started rethinking risk allocation and de-risking measures. Subsequently, two major reforms were introduced. First, for a market suffering from liquidity crises, a de-risked hybrid annuity model was launched. Second, investment conduits such as infrastructure investment trusts (InvITs) and toll-operate-transfer (TOT) models were introduced. These were the inflection points, wherein the highway ecosystem began to expand and diversify. While plain vanilla deals in the secondary market continued, InvITs and TOTs attracted international investors (private equity, pension funds, sovereign wealth funds and strategics). Such investments freed up equity for primary market players/engineering, procurement and construction (EPC) players. When unlocked, the capital was then recycled by the private sector into newer projects.

In terms of industry dynamics, players became more specialised and segmented. The growing ecosystem of operational assets and success stories gave rise to a variety of domestic players. First, prominent operation and maintenance (O&M) players emerged. These players could now provide services to investors who lacked O&M capabilities. Certain developers/EPC players saw the play of platforms and started building their own platforms, often by picking up assets early in the primary market itself, which includes construction risk. Smaller players who thrived as sub-contractors to the industry majors now aspired to become full-fledged EPC players, providing EPC services to developers.

operational assets and success stories gave rise to a variety of domestic players. First, prominent operation and maintenance (O&M) players emerged. These players could now provide services to investors who lacked O&M capabilities. Certain developers/EPC players saw the play of platforms and started building their own platforms, often by picking up assets early in the primary market itself, which includes construction risk. Smaller players who thrived as sub-contractors to the industry majors now aspired to become full-fledged EPC players, providing EPC services to developers.

Finally, the highway sector underwent a digital transformation. First, there was the implementation of FASTag. Implementing electronic toll collection at the level that India needed would have been a nightmare for any country. However, India implemented it seamlessly, riding on the fintech revolution, with collections reaching approximately $6.5 billion in calendar year 2022 and accounting for a 95 per cent share in all toll transactions on national highways. Second, there was a significant growth in scientific and digital asset management capabilities. Third, there was the successful implementation of intelligent transportation systems across major corridors.

Demand-side transformation – asset or service?

Continuous improvement and sectoral reforms are essential to maintain the sector’s competitive edge and its global competitiveness. Logistics efficiency is being prominently emphasised under Gati Shakti. Although there are improvements, the highway sector has a lot to catch up on in terms of labour productivity, mechanisation, and digitalisation. Environmental, social and governance factors, as well as supply chain financing and green finance, are not a regular feature of this sector. O&M expenditure remains in the single digit within the sector, creating an investment sustainability concern. Legacy problems such as land acquisition and clearances still exist to a large extent. The solution to all these issues lies in transforming the underlying philosophy of the sector, shifting from the traditional “asset” focused approach to the adoption of “road-as-a-service” and a “customer” centric approach.

The top priority of any road sector agency in India is to build and maintain roads. Additionally, key performance indicators (KPIs) are often “asset” centric, which include measuring potholes, roughness index and service levels.

A shift towards the “road-as-a-service” approach and customer centricity changes the basic construct of how the sector is strategised and managed. This starts with identifying who your customers are. Let us take the freight and trucking industry as an example. The question then becomes: Do drivers need breakrooms across the road network for improved productivity and safer driving? Is there a need to establish more multi-modal logistics parks (MMLPs) or warehouses across the network to help reduce logistics costs and turn-around time? Instead of raising speed limits, which can compromise safety, should we build dedicated freight lanes for mid-mile trips? Consequently, the KPIs for the sector would shift in this direction, making the actions/solutions more directly focused on addressing the problems.

Such a shift can also yield positive spillovers in various ways. For instance, driver breakrooms can potentially improve the quality of life for drivers and reduce crashes, along with the value-at-risk associated with such crashes. Establishing warehousing and MMLPs can generate significant captive traffic (as well as diverted traffic) for the road stretch, boosting toll collection and presenting oxbow or idle land parcel monetisation avenues.

Supply-side transformation

So far, we have only talked about how demand generators (government institutions in the sector) have transformed and can transform. We need the private sector to transform to a large extent on the supply side as well. The National Infrastructure Pipeline (NIP) presented a potential opportunity of Rs 20 trillion in the road sector to be delivered by 2026. As per our estimates, the capacity of the sectoral players to cater to this demand falls within the range of Rs 13 trillion-Rs 14 trillion. The gap can be settled through:

- The emergence of new domestic/international players

- A steep growth in order book – beyond capacity bets

- Extension of the NIP achievement timeline by a few more years

We see a play of all three factors in the sector today, with the emergence of new players and the steep order book growth being particularly pronounced in many ways. In a sector where projects typically span two to three years, a book-to-bill ratio of four to five appears plausible and indicates sustainable growth prospects. However, over the past three years, there has been a significant increase in aggressive bidding in the highway sector, leading to the emergence of newer players with book-to-bill ratios sometimes exceeding 10. This is not sustainable if the “business-as-usual” approach to operations continues. There is ample evidence for why transformation within private sector players remains critical.

Disruptions due to the Covid-19 pandemic are likely to remain and thus, building resilience within companies is critical. In the aftermath of the pandemic in late 2020, we analysed approximately 800 companies in the construction space, comprising roads and other sectors. Predictions based on 2019-20 data (pre-Covid) using the Zmijewski score showed that approximately 16 per cent of companies were under financial stress, and it was feared that the Covid-19 pandemic could push many of these companies to bankruptcy. By the end of 2022, many of those companies underwent insolvency proceedings. Thus, finance transformation and treasury risk management remain critical pillars for building such resilience.

Disruptions due to the Covid-19 pandemic are likely to remain and thus, building resilience within companies is critical. In the aftermath of the pandemic in late 2020, we analysed approximately 800 companies in the construction space, comprising roads and other sectors. Predictions based on 2019-20 data (pre-Covid) using the Zmijewski score showed that approximately 16 per cent of companies were under financial stress, and it was feared that the Covid-19 pandemic could push many of these companies to bankruptcy. By the end of 2022, many of those companies underwent insolvency proceedings. Thus, finance transformation and treasury risk management remain critical pillars for building such resilience.

Volatility in commodity prices (e.g., steel, bitumen) is quite common. However, a significant number of players experienced challenges due to skyrocketing prices in some segments caused by the Russia-Ukraine war. Day-to-day challenges in procuring sundry items remain a struggle for many, often triggering unnecessary delays and contractual risks. Transforming supply chain and inventory planning remains a key aspect to be addressed.

Similarly, automation and mechanisation are other areas that can improve the resilience of companies and provide them with the speed to get things done. Without such a transformation, either the infrastructure built will show quality issues, or the companies will eventually face financial issues. Seemingly unsustainable order books can be managed if these transformations are planned and implemented timely.

Quick takeaways

India remains one of the largest and most mature markets in the highway sector. The transformation over the past two decades involved strategic and tactical innovations, leading to a vibrant ecosystem of investors, EPC companies, developers, O&M players, and banking and technology institutions.

The single most important pillar of government-side transformation remains deeply rooted in the underlying philosophy of strategising and managing the sector. The question today is whether we should continue to focus on an “asset”-centric mindset, or whether we should transition into a “road-as-a-service” mindset and customer-centricity. On the private side, the ecosystem is significantly evolved. However, there is a need for customised transformation programmes to build resilience within the industry.